Accounts receivable general ledger transaction example

Accounting cycle revolves around identifying transactions, making relevant journal entries, posting those journal entries to ledgers and preparing trial balances and financial statements from those ledgers.

A general ledger is the set of all accounts where accounts receivable general ledger transaction example entries are posted. It is the main database of accounting transactions and provides input for preparation of a trial balance and eventually a complete set of financial statements. While the general journal records debit and credit effects of accounting accounts receivable general ledger transaction example, the general ledger presents the cumulative view of those journal entries on the balance in each account.

Since general ledger hold all the historical journal entries, some key general ledger accounts become so complex that a separate ledger is needed to keep track of its transactions. In such a situation, it is necessary to create a subsidiary ledger to hold each customer account and include the grand total of that ledger in the general ledger.

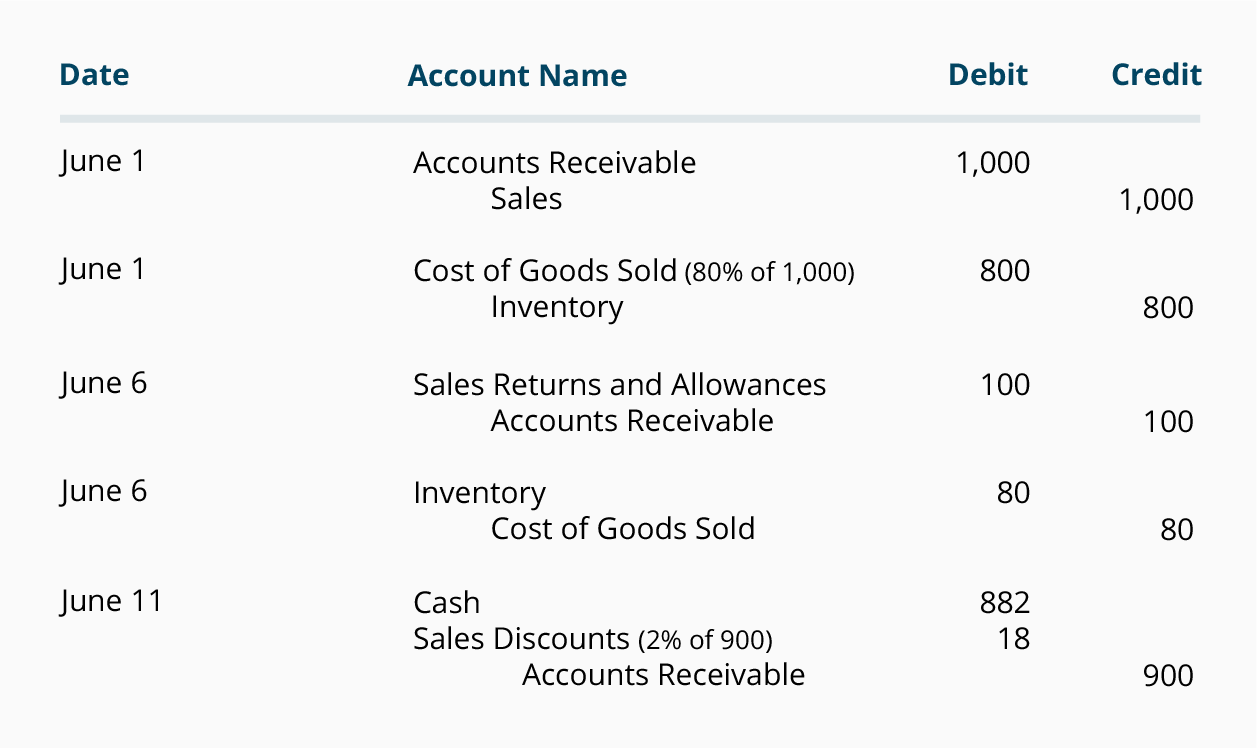

Mr C defaulted on his payments. At the end of the month, when cash is received and Mr. C defaults, following journal entries are posted to general ledger accounts:. Accounts receivable account included in the general ledger above is a control account, i. A subsidiary ledger is needed for accounts receivable control account because there are potentially thousands of accounts receivable transactions in a period and the subsidiary ledger makes it easier to keep track of those transactions.

Below is an except from accounts receivable subsidiary ledger showing entries made on 24 September At the end of the month when payment is accounts receivable general ledger transaction example and Mr. C defaults, following entries are made in the subsidiary ledger:. Accounts payable subsidiary ledger and fixed assets subsidiary ledger are other commonly used subsidiary ledgers. Contact Us Privacy Policy Disclaimer. There are two types of accounting ledgers: General ledger A general ledger is the set of all accounts where journal entries are posted.

Subsidiary ledger Since general ledger hold all the historical journal entries, some key general ledger accounts become so complex that a separate ledger is needed to keep track of its transactions. Following are opening balances of relevant accounts: C defaults, following journal entries are posted to general ledger accounts: C defaults, following entries are made in the subsidiary ledger:

These records remain as a permanent track of the history of all financial transactions since day one of the life of your company. Your accounting system will have a number of subsidiary ledgers called sub-ledgers for items such as cash, accounts receivable, and accounts payable. All the entries that are entered called posted to these sub-ledgers will transact through the general ledger account. For example, when a credit sale posted in the account receivable sub-ledger turns into cash due to a payment, the transaction will be posted to the general ledger and the two cash and accounts receivable sub-ledgers as well.

There are times when items will go directly to the general ledger without any sub-ledger posting. These are primarily capital financial transactions that have no operational sub-ledgers. These may include items such as capital contributions, loan proceeds, loan repayments principaland proceeds from sale of assets. These items will be linked to your balance sheet but not to your profit and loss statement.

There are two main issues to understand when setting up the general ledger. One is their linkage to your financial reports, and the other is the establishment of opening balances.

The order of how the numerical balances appear is determined by the chart of accounts, but all entries that are entered will appear. The general ledger accrues the balances that make up the line items on these reports, and the changes are reflected in the profit and loss statement as well. The opening balances that are established on your general ledgers may not always be zero as you might accounts receivable general ledger transaction example. On the asset side, you will have all tangible assets the value of all machinery, equipment, and inventory that is available as well as any cash that has been invested as working capital.

On the liability side, you will have any bank or stockholder loans that were used, as well as trade credit or lease payments that you may have secured in order to start the company. You accounts receivable general ledger transaction example also increase your stockholder equity in the amount you have invested, but not loaned to, the business. Feeding the hub information are the spokes of the wheel. These modules are ledgers themselves. We call them sub-ledgers. Each contains the detailed entries of its specific field, such as accounts receivable.

The sub-ledgers summarize the entries, then sends the summary up to the general ledger. For example, each day the receivables sub-ledger records all credit sales and accounts receivable general ledger transaction example received. If it doesn't, then there's accounts receivable general ledger transaction example problem.

An example of such a direct entry would be the payment on a loan. The same concept of a sheet of paper holds for each sub-ledger that feeds the general ledger.

A computerized accounting system works the same way, except that the general ledger and sub-ledgers are computer files instead of sheets of paper. There are a few and only a few things you need to understand in order to make setting up your accounting system easier.

They're basic trust meand they will probably clear up any confusion you may have had in the past when talking with your CPA or other technical accounting accounts receivable general ledger transaction example. These are the backbone of any accounting system. Understand how debits and credits work and you'll understand the whole system. Every accounting entry in the accounts receivable general ledger transaction example ledger contains both a debit and a credit.

Further, all debits must equal all credits. If they don't, the entry is out of balance. Out-of-balance entries throw your balance sheet out of balance.

Therefore, the accounting system must have a mechanism to ensure that all entries balance. Indeed, most automated accounting systems won't let you enter an out-of-balance entry-they'll just beep at you until you fix your error. Depending on what type of account you are dealing with, a debit or credit will either increase or decrease the account balance.

Here comes the hardest part of accounting for most beginners, so pay attention. Figure 1 illustrates the entries that increase or decrease each type of account. Notice that for every increase in one account, there is an opposite and equal decrease in another. That's what keeps the entry in balance. Also notice that debits always go on the left and credits on the right.

Notice how both parts of each entry balance? See how in the end, the receivables balance is back to zero? That's as it should be once the balance is paid. The net result is the same as if we conducted the whole transaction in cash:. Of course, there would probably be a period of time between the recording of the receivable and its collection.

Accounting doesn't really get much harder. Everything else is just a variation on the same theme. Make sure you understand debits and credits and how they increase and decrease each type of account. Balance sheet accounts are the assets and liabilities. When we set up your chart of accounts, there will be separate sections and numbering schemes for the assets and liabilities that make up the balance sheet. Increase assets with a debit and decrease them with a credit.

Increase liabilities with a credit and decrease them with a debit. Simply stated, assets are those things of value that your company owns. The cash in your bank account is an asset. So is the company car you drive. Assets are the objects, rights and claims owned by and having value for the firm.

Since your company has a right to the future collection of money, accounts receivable are an asset-probably a major asset, at that. The machinery on accounts receivable general ledger transaction example production floor is also an asset.

If your firm owns real estate or other tangible property, those are considered assets as well. If you were a bank, the loans you make would be considered assets since they represent a right of future collection. There may also be intangible assets owned by your company. Patents, the exclusive right to use a trademark, and goodwill from the acquisition of another company are such intangible assets.

Their value can be somewhat hazy. Generally, the value of intangible assets is whatever both parties agree to when the assets are created.

In the case of a patent, the value is often accounts receivable general ledger transaction example to its development costs. Goodwill is often the difference between the purchase price of a company and the value of the assets acquired net of accumulated depreciation.

Think of liabilities as the opposite of assets. These are the obligations of one company to another. Accounts payable accounts receivable general ledger transaction example liabilities, since they represent your company's future duty to pay a vendor. So is the loan you took from your bank.

If you were a bank, your customer's deposits would be a liability, since they represent future claims against the bank. We segregate liabilities into short-term and long-term categories on the balance sheet. This division is nothing more than separating those liabilities scheduled for payment within the next accounting period usually the next twelve months from those not to be paid until later.

We often separate debt like this. It gives readers a clearer picture of how much the company owes and when. After the liability section in both the chart of accounts and the balance sheet comes owners' equity. This is the difference between assets and liabilities. Hopefully, its positive-assets exceed liabilities and we have a positive owners' equity. In this section we'll put in things like.

Most automated accounting systems require identification of the retained earnings account. Many of them will beep at you if you don't do so. By the way, retained earnings are the accumulated profits from prior years. At the end of one accounting year, all the income and expense accounts are netted against one another, and a single number profit or loss for the year is moved into the retained earnings account. This is what belongs to the company's owners-that's why it's in the owners' equity section.

The income and expense accounts go to zero. That's how we're able to begin the new year with a clean slate against which to track income and expense. The balance sheet, on the other hand, does not get zeroed out at year-end. The balance in each asset, liability, and owners' equity accounts rolls into the next accounts receivable general ledger transaction example. So the ending balance of one year becomes the beginning balance of the next. Think of the balance sheet as today's snapshot of the assets and liabilities the company has acquired since the first day of business.

The income statement, in contrast, is a summation of the income and expenses from the first day of this accounting period probably from the beginning of this fiscal year.

Further down in the chart of accounts usually after the owners' equity section come the income and expense accounts. Most companies want to keep track of just where they get income and where it goes, and these accounts tell you.

For income accounts, accounts receivable general ledger transaction example credits to increase them and debits to decrease them.

For expense accounts, use debits to increase them and credits to decrease them. If you have several lines of business, you'll probably want to establish an income account for each. In that way, you can identify exactly where your income is coming from.

Open topic with navigation. This topic provides additional information on the basic setup of receivable accounts, why actions taken have different affects on account balances, and how data flows from the Tenant Accounts Receivable program to the General Ledger program. Within any accounting system, there accounts receivable general ledger transaction example what is referred to as the General Ledger. This is a tracking system designed to accumulate financial monetary information, group the financial information by type or category of similar transactions, and provide a means of reporting this information in standardized formats.

This topic defines the basic series of transactions and processes that normally occur in a housing agency HA. Hopefully, this will help you understand the basic setup of receivable accounts, why actions taken have different affects on the account balances, and how the data flows from the Tenant Accounts Receivable TAR program to the General Ledger GL program. Manually selecting the account for each side of the transaction, resulting in a balanced entry. In Setup, these are pre-selected accounts that a transaction can use to allocate the dollar amounts to multiple accounts within the ledger based on a percentage value.

Within each HA operation, there are several different funds. Each fund is defined by the source of funds available for use and the restrictions placed on the use of these funds. Accounting for the assets, liabilities, cash receipts, and disbursements is completely separate within each fund. It is customary for an HA, in order to simplify the accounting and record keeping functions, to receive and disburse all cash from a single bank account.

This necessitates additional accounting to reflect the amount of cash received or disbursed from one fund that actually belongs to another fund. Examples of funds are:. The record of the income at the time of the charge, usually used when an amount due from the tenant for services rendered is not already on their account; for example, rent, work order charges, utilities. A receivable is added to an account to show an amount due without actually affecting the account balance.

Internal transfers between accounts or transfers to another program such as Accounts Payable for a refund request. Shows the amount due, but does not change any balances until the amount due is collected or paid. Charge a tenant for rent, services, late fees or basically accounts receivable general ledger transaction example Tenant makes a payment: Creates an entry to decrease credit the amount the tenant owes on the associated receivable account and increase debit the amount of money held in the cash drawer physical drawer, desk, box or where the money is kept until the deposit is made.

Charging a tenant and a tenant making a payment require different GL account numbers. Failure to use different account numbers for cash in the bank and for the cash drawer will result in incorrectly dated entries in GL's cash in bank account and, ultimately, no cash flow integrity. Decreases credits the cash drawer account and increases debits the cash in the bank account. Credit Memo to remove a previous charge: Creates entries in GL that are the reverse of the original charge function.

Transfer of balances from one account to another: As an account is accounts receivable general ledger transaction example detailed listing of transactions that add up to the balance in GL, any transfer of the transactions or balance in the account to another account also requires corresponding transactions in GL to reflect this transfer.

Tenant owes on escrow account: Use a receivable action to show the amount due, but not to change the balance on the escrow account until the payment is actually made. This action does not, by itself, create any journal transactions in GL.

It does, however, transfer the amounts and appropriate GL account numbers to Accounts Payable to generate a check to affect the refund. This check then creates the journal entry that records refund request action. Public Housing tenant signs up for FSS program: When the tenant qualifies for a transfer of rent paid into the FSS escrow account, there are specific transactions and actions used to record this function.

The first three steps are completed at the beginning of each month. The fourth step, which is the payment, is completed when it is received:. Below is a description of the series of transactions that occur with this action and how each of these transactions are then recorded in GL as a balanced entry as a credit and a debit. Payments, deposits, NSF checks, write-offs, transfers to other types of accounts, security deposit payments, refunds, other types of charges, are examples of the transaction types found in TAR.

The series of transactions are the same as listed above, just with different descriptions, and each series of transactions that are recorded in GL have to be a balanced entry credit and debit.

Consider where the money is coming from. It eventually comes from the tenant, but, why? You are charging rent, so the money is coming from rent charges or rent income or dwelling rental revenue.

Consider where the money is going. The tenant is not actually paying, you are just charging the tenant for something they will pay. Thus, we are increasing the amount of receivable from the tenant, or tenant accounts receivable. Consider how to properly record charging rent in General Ledger.

On one side of the balanced entry, you credit the amount represented by a negative sign to the dwelling rental income since this is where the money is coming from. Then, add the amount to the balance already on the account to arrive at the total to date amount. On the other side of the balanced entry, you debit the amount represented by a plus sign to tenant accounts receivable since this is where the money is going.

Again, add the amount to the balance already on the account for a total to date amount. The date of the transaction is Juneand the reference, or description, of this transaction should describe what is happening; i. The master account that all customers have. This type of account records charges and payments. Each charge accounts receivable general ledger transaction example the account is due in full as of the date of the charge.

Periodic payments are allowed, but any charge not paid or credited off is past due as soon as the charge date is passed. An escrow account is a security deposit, pet deposit, FSS escrow account, or other account where the value on the account accumulates or increases as payments are made into the account.

There are no charges, thus no transactions associated with this type of account. The user may set up a receivable not a chargeto show how much the tenant should be paying, but receivables are not accounts receivable general ledger transaction example with any GL account number.

Thus, escrow accounts do not create a journal transaction. The payment, however, does create a transaction which credits the accounts receivable general ledger transaction example and debits the cash drawer. The balance of the escrow account continues to accumulate as a negative balance to show that the HA owes the tenant the amount reflected in the account.

This is a repayment agreement type accounts receivable general ledger transaction example. Amounts charged on the primary accounts receivable account are transferred to this account and this transfers the balance due. Then, recurring receivable amounts are defined for the monthly payment amounts that should accounts receivable general ledger transaction example paid to reduce the overall balance due. There are no transactions accounts receivable general ledger transaction example with this account as all charge items have already been recorded on the AR account and transferred.

This account type is similar to the revolving credit account in setup and actions.